Do I Enter My Whole Family's Income for Household Income if I Am an Adult Living With Parents

Financial eligibility for most categories of Medicaid and the Children'due south Health Insurance Programme (CHIP) is determined using a tax-based mensurate of income called modified adjusted gross income (MAGI). The MAGI methodology includes rules prescribing who must be included in a household when determining eligibility. The following Q&A explains MAGI and the rules for determining Medicaid and Flake households under MAGI.

↓ Download PDF

What is MAGI?

MAGI is a methodology used to determine income for the purposes of Medicaid or Scrap eligibility. It is based on taxation definitions of income and household. MAGI rules for determining what income to count when determining Medicaid, Flake, and premium tax credit eligibility are mostly aligned. The rules determining who is in a household and whose income to count, even so, can vary significantly. Too, under MAGI rules, an individual or family's avails do not count in determining eligibility. (For more information on what income counts under MAGI rules, see Key Facts: Income Definitions for Marketplace and Medicaid Coverage.)

To whom do the MAGI rules employ?

All states must apply the MAGI rules regardless of the decision to expand Medicaid. However, MAGI rules employ only to certain categories of Medicaid eligibility. These include parents and caregiver relatives, children, pregnant women, and the adult expansion grouping. States' previous rules for determining income and households continue to apply to the elderly, disabled, and children in foster care.

How practise Medicaid and premium taxation credit household rules differ?

Medicaid and Bit households are determined based on a person's family and tax relationships as well every bit their living arrangements. How people file taxes and who is in their tax unit of measurement doesn't ever determine who is in their Medicaid household, but it determines which Medicaid household rules apply in defining the household. Premium revenue enhancement credit household rules, on the other hand, are based purely on tax relationships.

The most important difference between Medicaid and premium tax credit households is that for Medicaid, household size and composition are determined separately for each member of the household, but for the premium revenue enhancement credit, members of a tax unit are e'er treated as a household. This means that for Medicaid, household size may differ for family members even when they are in the same tax filing household. Thus, it is possible that for Medicaid, a family unit of iii filing its taxes together may have two members with a household size of 3 and the tertiary member of the family may be a household of ane. For the premium tax credit, each fellow member of a household that files its taxes together will take the same household size. (For more information on determining household size for the premium revenue enhancement credit, see Key Facts: Determining Household Size for the Premium Revenue enhancement Credit.)

Another important difference is Medicaid provides states with several options that affect how they define households when determining Medicaid eligibility. Nonetheless, because the premium tax credit is a federal benefit, the rules are established at the federal level and are consistent across states.

How does Medicaid decide who is in a household?

Medicaid determines an individual's household based on their plan to file a tax render, regardless of whether or not he or she actual files a return at the cease of the twelvemonth. Medicaid likewise does not require people to file a federal income tax return in previous years.

For each private applying for coverage, Medicaid looks at whether he or she plans to exist:

- a tax filer

- a revenue enhancement dependent

- neither a tax filer nor a dependent

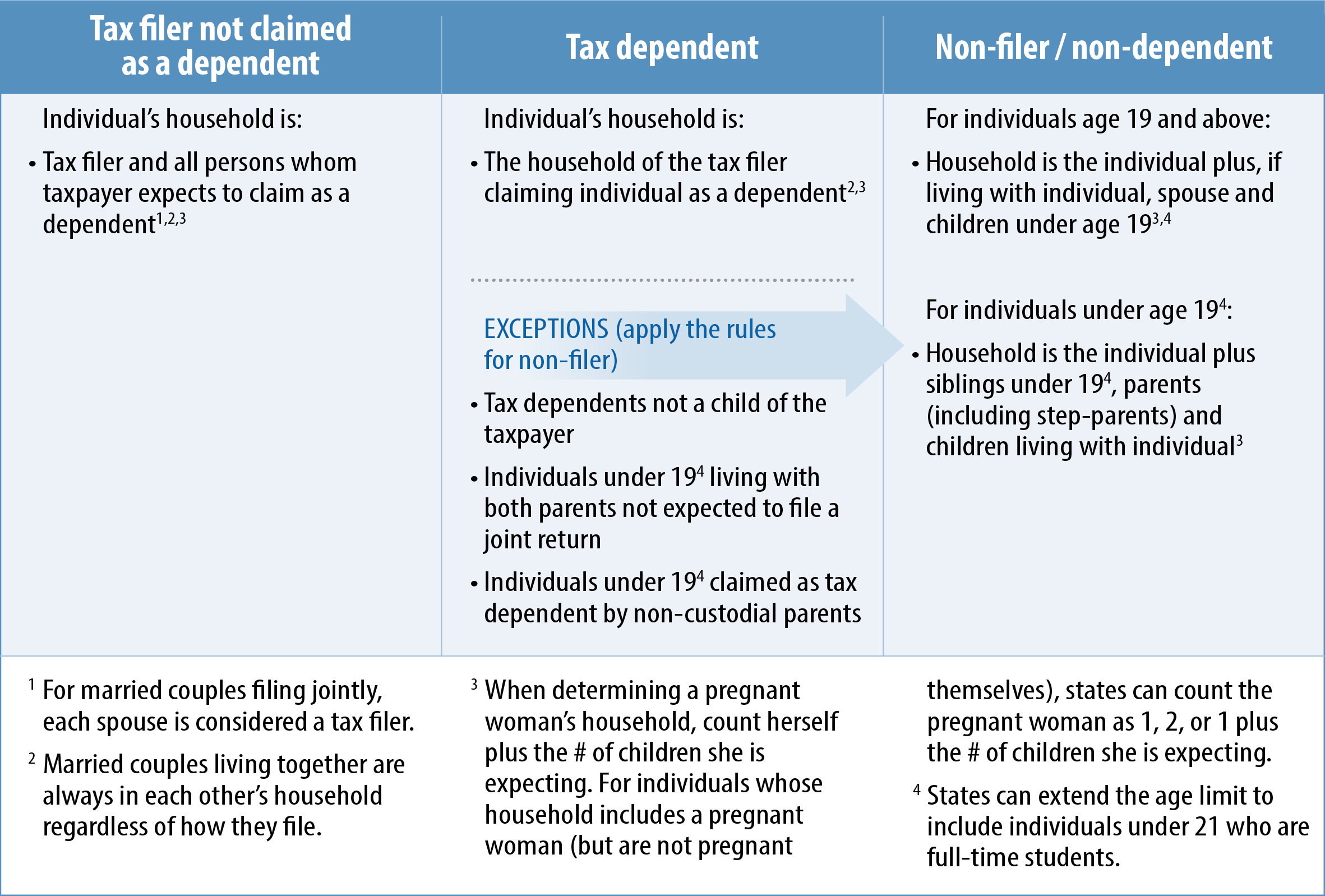

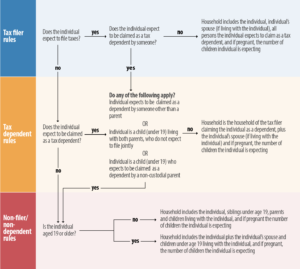

People'southward intended tax filing status determines which Medicaid household rules utilise in making the household determination. Figure 1 summarizes the Medicaid household rules and Effigy 2 shows how to apply these rules. (For more information, see Reference Guide: Medicaid Household Rules.)

| FIGURE 1: MAGI Rules for Determining Medicaid and CHIP Households | ||

| ||

| Effigy two: How to Determine An Private'south Medicaid Household | ||

| ||

What are the household rules for a tax filer?

For tax filers claiming their own exemption and who can't exist claimed as a tax dependent, the household includes the tax filer, the spouse filing jointly, and everyone whom the tax filer claims as a tax dependent.

What are the household rules for tax dependents?

For tax dependents, the household is the aforementioned as the taxation filer claiming the individual every bit a revenue enhancement dependent. However, there are three exceptions to this rule, when the rule for not-filers is applied:

- Individuals who expect to be claimed every bit a dependent by someone other than a parent;

- Individuals (under xix) living with both parents, whose parents do non expect to file a joint tax return; and

- Individuals (under 19) who expect to exist claimed as a dependent by a non-custodial parent.

What are the household rules for people who neither file a tax render nor are claimed as a tax dependent?

For individuals who neither file a taxation return nor are claimed as a tax dependent, the household rules differ based on whether the private is an adult or a pocket-size:

- For individuals 19 years and older, the household includes the individual plus, if living with the private, his or her spouse and children who are under 19 years quondam.

- For individuals nether 19 years old, the household includes the private, plus any siblings under 19 years quondam, children of the individual and parents who live with the private.

Are there any adjustments to the iii rules based on people'southward revenue enhancement filing?

In improver to the general rules for determining household size, some rules apply in all situations:

- Married couples who alive together are e'er counted in each other'south household regardless of whether they file a joint or separate return.

- Family size adjustments need to be made if the private is pregnant. In determining the household of a pregnant adult female, she is counted as herself plus the number of children she is expected to evangelize.

What are different options that states accept for implementing MAGI?

States have flexibility in how they implement the MAGI rules in two areas. Starting time, in some instances the Medicaid household rules practical may depend on whether an private is under 19 years old or not. Where the rules indicate an historic period limit, states have the option to extend that age limit to 21 if the individual is a total-time educatee. 2d, for individuals whose household includes a meaning woman (just are non pregnant themselves), states can count the meaning woman as one, ii, or one plus the number of children she is expecting.

Are married couples who file taxes separately considered to be in carve up households?

Mostly, no. Married couples who live together are e'er considered to be in each other's household regardless of how they file taxes.

Even so, married couples who don't live together and who file taxes separately will exist considered as separate households.

How does Medicaid decide the household size of family members when the parents alive together but are non married?

Every bit long every bit both parents file taxes, non-married parents living in the same household would still apply the rule for revenue enhancement filers to decide each parent'southward Medicaid household. This ways their household includes themselves and anyone claimed equally a dependent on their tax return.

However, a kid nether nineteen living with not-married parents and being claimed every bit a taxation dependent by i of the parents, would autumn into the not-filer rule. Therefore, the kid's household size for Medicaid would include himself, both parents, and any siblings living with the child. For instance:

- Dan and Jen alive together with their two children, Drew and Mary. Considering they are not married, Dan and Jen must file dissever returns. Jen claims Drew and Mary as tax dependents on her taxation return. Dan files equally a single person and doesn't merits whatsoever taxation dependents. Table i illustrates the household size determination for each fellow member of the family. To determine the household size for Dan and Jen, Medicaid would apply the taxation filer rule and include everyone in each of their specific tax household. To make up one's mind the household size for Drew and Mary, Medicaid would apply the non-filer rule because they are children living with both parents who are not expected to file a articulation render.

| TABLE 1: Example of Determining Households for Not-Married Parents | |||||||

| Filing Status | Counted in Household | Household Size | Medicaid Rule Applied | ||||

| Dan | Jen | Drew | Mary | ||||

| Dan | Tax filer | X | i | Tax filer rule | |||

| Jen | Tax filer | X | X | Ten | iii | Taxation filer rule | |

| Drew | Revenue enhancement dependent | X | X | Ten | X | 4 | Non-filer dominion (exception) |

| Mary | Revenue enhancement dependent | X | X | X | X | iv | Non-filer rule (exception) |

How does Medicaid determine the household of an developed child who is claimed as a tax dependent by his parents?

The household of an individual who is at to the lowest degree 19 years old and is claimed equally a tax dependent by his parents is always the same every bit the household of the parents claiming him. This is true even if the individual was much older, say 35 years former. For case, under some circumstances parents can merits their kid who is 35 years old as a qualifying relative on their tax return. In this scenario, Medicaid would utilise the tax dependent rule for determining the household of this individual, which means his household would exist the same equally the household of his parent (the tax filer) claiming him as a dependent. The post-obit examples illustrate how the Medicaid rules would be applied:

- Barry is 29 and is claimed equally a tax dependent by his parents. His parents likewise claim Barry's younger brother and sister, who are 15 and 17. When determining his household for Medicaid, Barry has the same household every bit the tax filer challenge him equally a dependent, thus Barry would have a household size of v: himself, both of his parents, and his brother and sister.

- Carla is 28 years and lives with both parents who are married. However, her parents file split taxation returns and Carla'southward begetter claims her every bit a dependent on his taxation return. Even though Carla'south parents file split up returns, married people living together are e'er in the same household as their spouse. As a result, Carla's male parent has a household of iii: himself, his spouse, and Carla. This means that Carla besides has a household of three.

Does the exception to the tax dependent dominion for revenue enhancement dependents who are not a child of the taxpayer only apply to adult revenue enhancement dependents?

No. This exception also applies to minors claimed as a revenue enhancement dependent past someone other than their parent. Anytime an individual — regardless of age — is claimed as a tax dependent by someone other than their parents, the non-filer rules utilise in determining that private's household. For example:

- Leena lives with and is nether the guardianship of her aunt. She is five years one-time and doesn't have any siblings or parents living with her. Leena's aunt claims her as a qualifying relative on her tax return. Leena is a tax dependent but she falls under one of the exceptions to the revenue enhancement dependent dominion because she is not the tax dependent of her parents. This means Medicaid will use the not-filer rules to determine her household, and as a result, Leena's household consists only of herself.

View all key facts

Source: https://www.healthreformbeyondthebasics.org/key-facts-determining-household-size-for-medicaid-and-chip/

{kind=link}

Post a Comment for "Do I Enter My Whole Family's Income for Household Income if I Am an Adult Living With Parents"